Revisiting Dryships’ 2019 Take-Private: NAV Arbitrage vs. Timing the Cycle

You’ve probably heard this one before: An economist and his friend are walking down the street when they see a $20 bill lying on the ground. The friend bends down to pick it up but the economist says, “Don’t bother. If it were real, someone would have already picked it up.”

Here’s another variation: An investment analyst researching the shipping industry notices that a public shipping company trades at a steep discount to their net asset value (NAV) and suggests taking it private to his boss. The usual responses are the same as the one in the joke. If the value was there to be captured, somebody else would have done it already.

However, there is one example of a shipowner who decided to stop and pick up that $20 he saw lying around on Wall Street – George Economou. Economou took his shipping company, DryShips Inc., public on the NASDAQ in 2005.

DryShips then had a rollercoaster ride in the public capital markets–it benefited from the booming dry bulk shipping market; suffered through the lean years following the 2008 financial crisis; entered into a series of dilutive equity issues and reverse stock splits; built up a following amongst retail investors attracted by the stock's volatility; and incubated and spun off an offshore drilling company, Ocean Rig.

As the dry bulk market began to stabilize after bottoming out in 2016, DryShips began growing its fleet and amassing a sizable cash pile from its earnings.

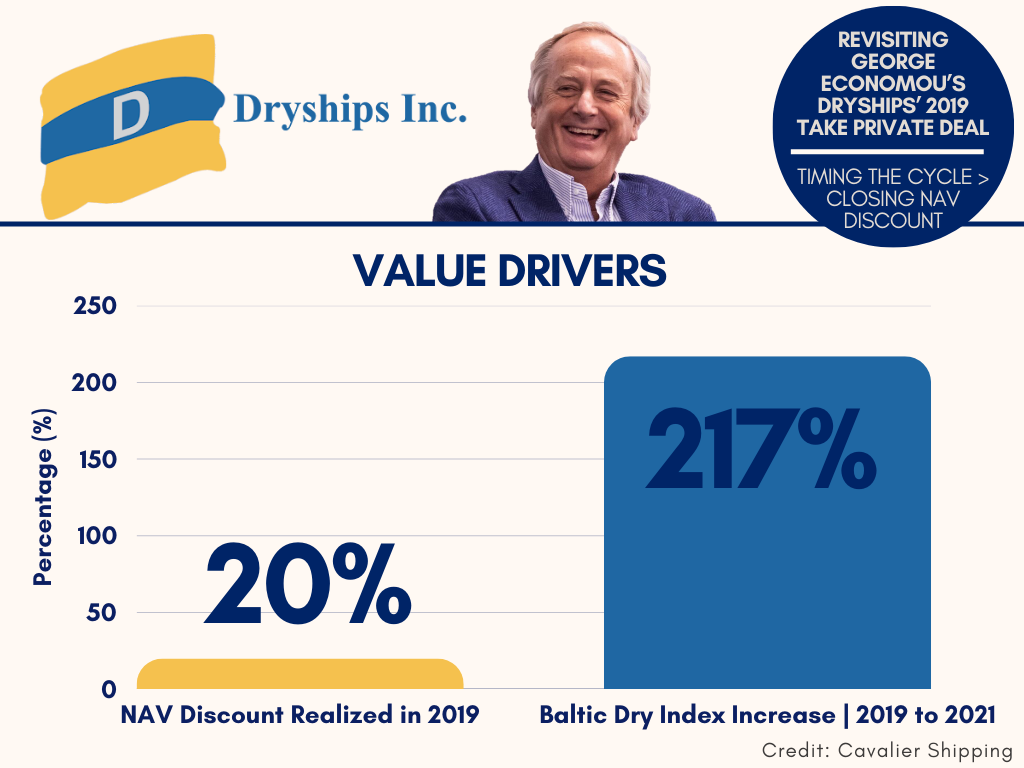

In 2019, DryShips was trading at a price to net asset value (P/NAV) of less than 0.50x. Economou decided it was time to buy out all of the shares he didn’t already own at a price equal to approximately 0.8x P/NAV. This was a material increase of almost 60% from where the shares had been trading prior to his offer, but still represented a 20% discount from the underlying NAV.

In hindsight, this ended up being an incredibly successful deal for Economou. But it wasn’t because he successfully arbitraged his discounted share price. It was because the shipping markets would proceed to go on a tear—the Baltic Dry Index would more than double from 2019 to 2021—and Economou was able to enjoy the spoils of that good market all to himself, without having to share with his minority public shareholders.